Most people think of gold or diamonds when they imagine Africa’s mining boom. Today, the continent is chasing something far more valuable: lithium, the key ingredient in electric-vehicle batteries and renewable-energy storage. As countries race to build a cleaner future, Africa has unexpectedly become the heart of the global supply chain—making it a crucial player in the shift away from fossil fuels. But like all gold rushes, this one comes with winners, losers, and serious risks.

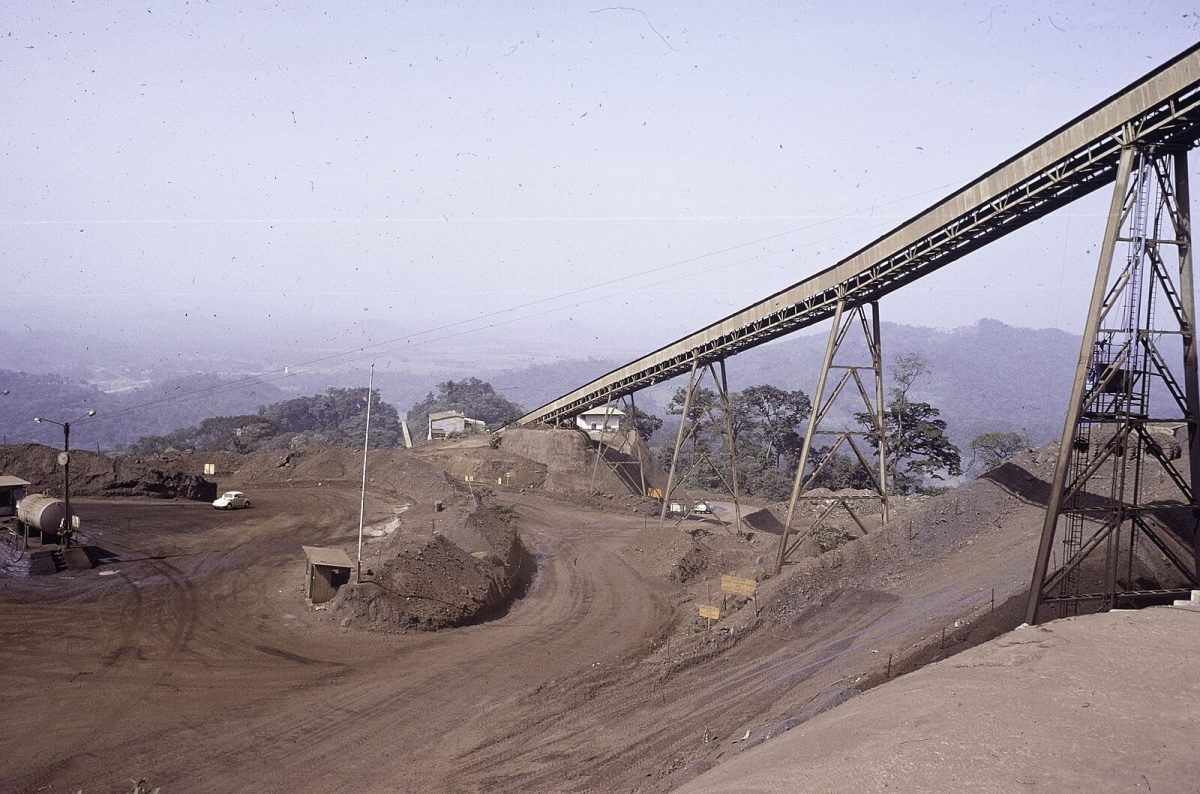

Demand for lithium has exploded as governments push for electric cars and large-scale battery storage. The European Union’s Critical Raw Materials Act labels lithium “strategic,” and China controls more than 65% of global refining. That means countries are scrambling to secure new sources, and Africa’s geology gives it a major advantage. Shallow deposits, lower extraction costs, and access to Atlantic and Indian Ocean ports have made Zimbabwe, Mali, Namibia, and the Democratic Republic of Congo central to the rush. Analysts expect Africa to record the fastest lithium supply growth of any region worldwide in 2025.

Zimbabwe shows how quickly the industry is changing. After banning raw ore exports in 2022 to force companies to process lithium locally, the government is now signaling a 2027 ban on exporting concentrates as well. The message is clear: if foreign companies want Africa’s minerals, they must invest in African value-add. But Zimbabwe still faces major hurdles, including power shortages and unstable infrastructure.

Mali’s Goulamina mine – backed by China’s Ganfeng Lithium—began shipments in 2025 despite security challenges. Another project, Bougouni, trucks thousands of tons of concentrate each month to Côte d’Ivoire’s San Pedro port. These operations highlight both the promise and fragility of Africa’s role: the resources are there, but logistics can be disrupted by unrest or border closures.

In the DRC, the massive Manono deposit remains tied up in lawsuits and political disputes, showing how governance issues can overshadow even world-class resources. Namibia, still early in development, has already drawn warnings from investigators about weak oversight and potential corruption.

Behind the boom is a global power struggle. China’s dominance in lithium processing means much of Africa’s output ultimately becomes “Chinese lithium” once refined. Western governments want to diversify supply chains, but they often struggle to match China’s investment speed. At the same time, African leaders are increasingly embracing “resource nationalism,” insisting that minerals contribute more to local economies – not just foreign industries.

But the rush comes with consequences. Mining strains water supplies, threatens wildlife habitats, and raises concerns about worker protections. Without strong oversight, “green” minerals could carry the same social and environmental costs as older extractive industries. Communities fear that, once again, wealth will leave and problems will stay.

Africa’s lithium boom offers the continent a rare chance to shape the future of global energy. Whether it becomes a story of empowerment or exploitation depends on what happens next – because in this new gold rush, the stakes are far higher than precious metals.